Treatment of Cash Received from Trade Receivable via Electronic Transfer on Reporting Date

Background:

All cash transfers made via the electronic transfer system are deposited in the recipient’s bank account two working days after they are initiated by the payer.

An entity has a trade receivable with a customer. At the entity’s reporting date, the customer has initiated a cash transfer via electronic transfer to settle the trade receivable. The entity receives the cash in its bank account two days after its reporting date.

Query:

Whether the entity should derecognize the trade receivable and recognize cash on the date the cash transfer is initiated (its reporting date), rather than on the date the cash transfer is settled (after its reporting date)?

Response:

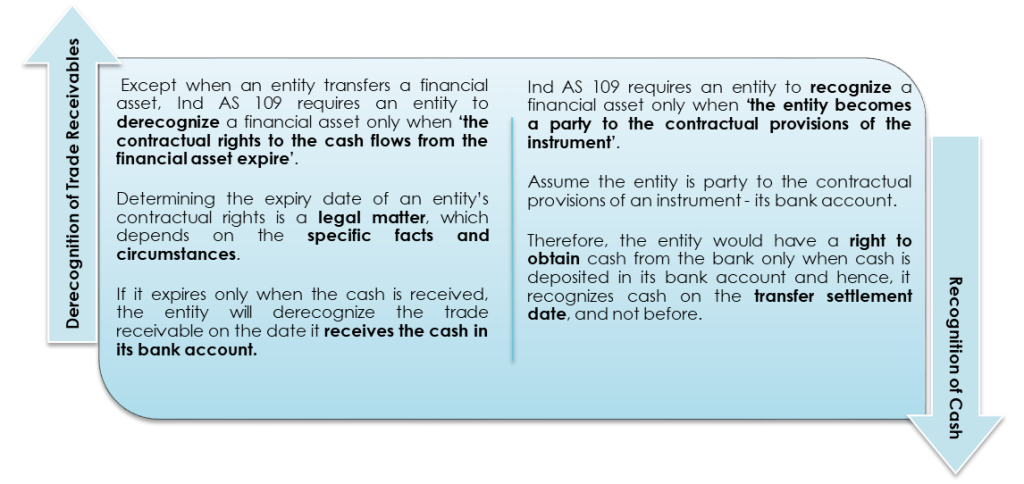

The entity is neither purchasing nor selling a financial asset. Therefore, o the provisions of Ind AS 109 specifying requirements for a regular way purchase or sale of a financial asset are not applicable; rather o the provisions relating to derecognition of trade receivable and recognition of cash as a financial asset are applicable.

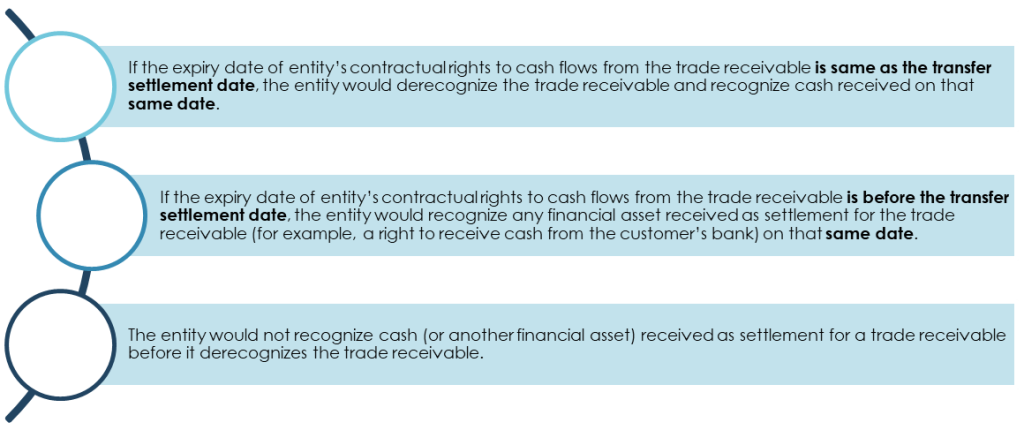

Depending upon the date on which the “contractual rights to cash flows from the trade receivable expire” and the date on which “cash is deposited in its bank account”, the following scenarios are possible:

The above is based on International Financial Reporting Interpretations Committee (IFRIC)’s tentative agenda decision.

SW Point of View:

Applying paragraphs 3.2.3 and 3.1.1 of Ind AS 109, the entity:

derecognizes the trade receivable on the date on which its contractual rights to the cash flows from the trade receivable expire; and

recognizes the cash (or another financial asset) received as settlement for that trade receivable on the same date.