Schedule III of The Companies Act, 2013 requires the presentation of ‘Trade Receivables’ as a separate line item on the face of the Balance Sheet under ‘Current Assets’, which should be further categorized into:

Earlier, there was no requirement of disclosing the ageing of trade receivables beyond the period of 6 months and only total balances were to be categorized as due for more than 6 months and others required to be disclosed. There was also no requirement of disclosing disputed dues out of total amounts of trade payables.

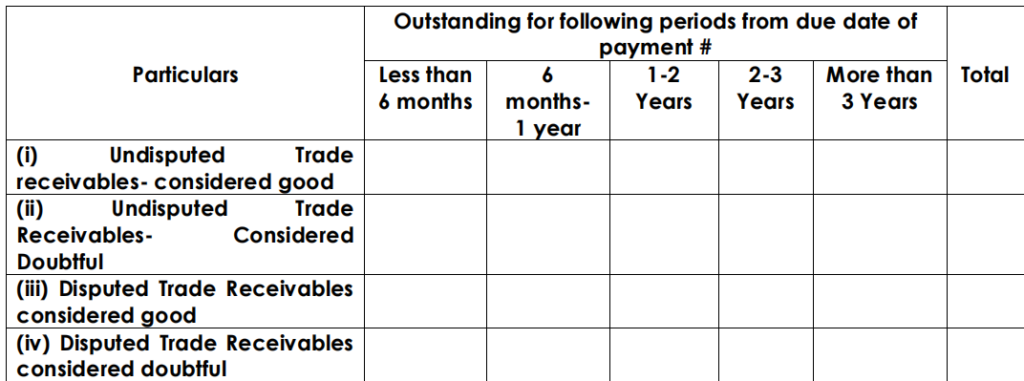

As per the amended Schedule, companies are now required to disclose an ageing schedule in respect of trade receivables in the following format:

# Similar information shall be given where no due date of payment is specified in that case disclosure shall be from the date of the transaction.

This additional disclosure requirement will result in transparency and quality of disclosures of trade receivables because it provides broad indicators of the health of the trade receivables portfolio of a company, which is generally a significant component of the balance sheet for all stakeholders of the company, including potential and existing investors, lenders and analysts.

The above disclosure shall be made by all the companies preparing Financial Statements as per Companies (Accounting Standards) Rules, 2021 for the financial year 2021-22 onwards.