A. Introduction

The IFRS Interpretations Committee (“Committee”) met on 29 November 2022. The Committee discussed matters that have been raised as possible amendments in the next annual improvements cycle. The Committee provided advice on the recommendation to amend various IFRS, but in this update we will going to discuss IFRS 10’s ‘De facto agent’ assessment amendment in detail.

B. Proposed Amendments

The Committee provided advice on the recommendation to delete particular wording which has been strikethrough below in paragraph B74 of IFRS 10 that has created the inconsistency with paragraph B73.

C. Facts

Paragraphs B73–B74 state:

B73 – When assessing control, an investor shall consider the nature of its relationship with other parties and whether those other parties are acting on the investor’s behalf (i.e., they are ‘de facto agents’). The determination of whether other parties are acting as de facto agents requires judgement, considering not only the nature of the relationship but also how those parties interact with each other and the investor.

B74 – Such a relationship need not involve a contractual arrangement. A party is a de facto agent when the investor has, or those that direct the activities of the investor have, the ability to direct that party to act on the investor’s behalf. In these circumstances, the investor shall consider its de facto agent’s decision-making rights and its indirect exposure, or rights, to variable returns through the de facto agent together with its own when assessing control of an investee.

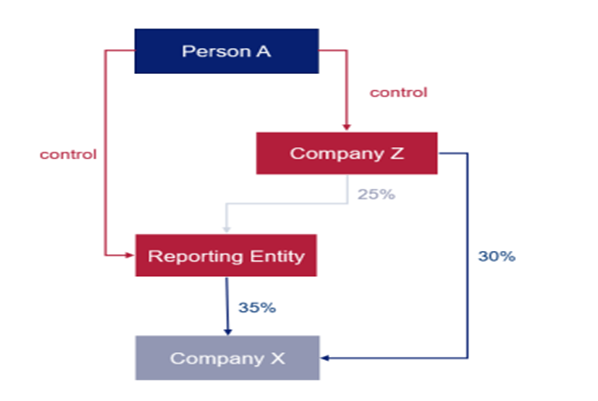

The below example would help us to understand confusion,

In the above figure, we can conclude that Person A controls both Company Z and Reporting Entity. Person A therefore has the ability (a) to direct Company Z to act on behalf of Reporting Entity, and (b) to direct Reporting Entity to act on behalf of Company Z. If we assume that both Reporting Entity and Company Z were required to prepare financial statements that comply with IFRS Accounting Standards, applying paragraph B74:

(a) Reporting Entity would conclude that it controls Company X. This is because it would consider both Company Z’s decision-making rights and its indirect exposure, or rights, to variable returns from Company X together with its own when assessing control of Company X; and

(b) Company Z would conclude that it controls Company X for the same reason. It would consider both Reporting Entity’s decision-making rights and its indirect exposure, or rights, to variable returns from Company X together with its own when assessing control of Company X.

Therefore, applying paragraph B74 both Reporting Entity and Company Z would conclude that they control Company X, which contradicts the IASB’s view when it developed IFRS 10. As stated in paragraph BC69 of the Basis for Conclusions on IFRS 10, the IASB confirmed that only one party, if any, can control an investee.

SW’s Remarks:

Committee has proposed this amendment to ensure that investee is being controlled by one party who can direct investee’s actions. Agenda papers for this proposed amendments are available on the IASB’s website for the general public. There are some more amendments proposed in other IFRS which will be covered in the further upcoming updates.