The Policy Branch of Trade and Taxes, Delhi has issued instructions for their field formations. The branch received various representations from taxpayers who are not allowed to get mistakes corrected on an order “that are apparent on record”. The branch observed that there are provisions in the Law to make such corrections, yet those were not followed and taxpayers are compelled to litigate issues by following complex procedures.

As per Section 161 of the CGST Act, 2017, rectification orders can be issued on being notified by the proper officer of the GST or on an application of the taxpayer. Application for rectification should be filed within three months of date of issuance of the order or notice and rectification order must be passed within six months. Said six months shall not apply in case of clerical or arithmetical errors, arising from any accidental slips or omissions.

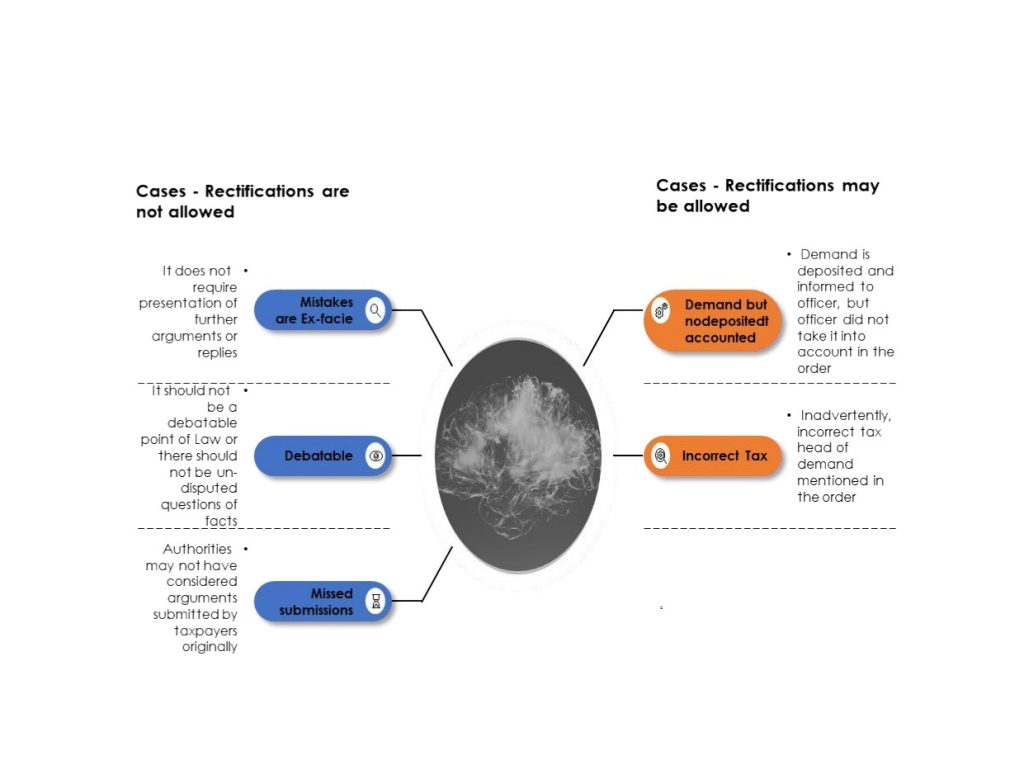

Instructions provided certain examples of mistakes apparent from record, as illustrated below:

| SW Point of View: By these instructions policy branch intends to educate industry and proper officers on provisions provided in the Law about rectifications of mistakes that are apparent from record. A good intent! |

Samyak Jain, Indirect Tax, SW India

Source: Notification F.No. 3(543)GST/POLICY/2024/1312-18 dated 01.03.2024