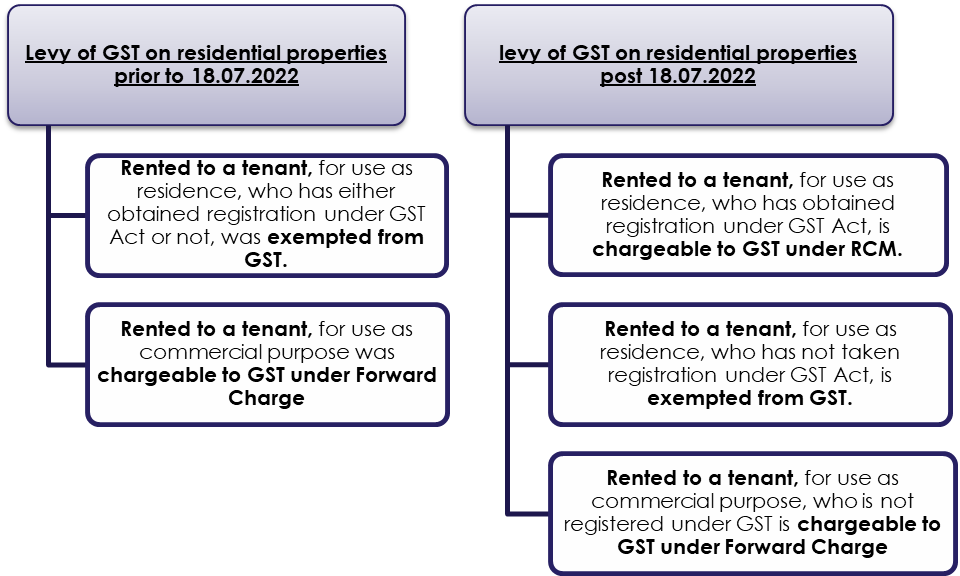

GST on residential properties prior to 18.07.202

Service by way of renting of residential dwelling for use as residence was exempted from GST vide entry no. 12 of notification no. 12/2017 dated 28.06.2017, as amended from time to time. These services were also exempted during the Service Tax regime and the same intent was carried forward under GST regime.\

GST on residential properties post 18.07.2022

Exemption on renting of residential dwellings stands withdrawn with effect from 18.07.2022, for specified persons. Now onwards, if residential dwelling is let out to a person, who has GST registration, will be subject to levy of GST on rent paid under reverse charge mechanism (RCM) basis. Residential dwelling let out to a person who has not obtained a GST registration, continues to be exempt from GST on RCM basis.

Government has shifted the responsibility of paying GST on the tenant under RCM vide entry no. 5AA of notification no. 05/2022 dated 13.07.2022.

Admissibility of ITC of GST paid under RCM

Provisions to avail input tax credit are given under chapter V of the CGST Act, 2017. Inter-alia, provide that GST credit shall not be admissible when goods or services or both are used for personal consumption. Principally the tenant would be using the property for its residence, which is a personal item, therefore GST credit would not be admissible. However, the tenant may take a view of taking GST credit attributed to the area or premises used or intended to be used by him for his professional / business use.

| Scenario | Is the tenant registered under the GST? | Has tenant obtained GST registration at the place of residence? | If no, has the tenant obtained GST registration at any other place but, in the same STATE? | If no, has the tenant obtained GST registration in any other STATE? | Are landlord and tenant members of the same family? | Applicability of GST Under RCM |

| 1* | No | – | – | – | No | No GST |

| 2 | Yes | Yes | – | – | No | GST is payable by the tenant under RCM. The place of supply would be intra-state. Tenant can avail of GST credit attributed to an area that he has used for his business or profession |

| 3 | Yes | No | Yes | – | No | GST is not payable by the tenant under RCM. Tenant cannot treat the said transaction as business expenditure in his books. However, CBIC should come up with more clarity for non-applicability of RCM under such situation because department may litigate on this and construe it to fall under ambit of RCM. |

| 4 | Yes | No | No | Yes | No | GST is not payable by the tenant under RCM. Tenant cannot treat the said transaction as business expenditure in his books. However, the CBIC should come up with more clarity for no applicability on RCM under such situation because department may try to litigate it and construe it to fall under ambit of RCM. |

| 5 | Yes | Either of the case | Yes | Since the transaction is between the related parties, therefore, GST is payable by tenant under RCM on a fair market value. |

*By virtue of this amendment, GST under RCM is payable only if a tenant is registered under GST. If a tenant is not registered under GST, he doesn’t have to obtain a GST registration under section 24 of the CGST Act. The taxability is not on service per se but to whom the services are provided, therefore, if tenant is not registered then there is no taxability on such renting services.

A. Entities other than individual, providing residential facilities to its employees. The residential facility can be given under terms of employment, due to relocation of the employee to a new State or due to any other reason. Based on the amendment, entities will now have to pay GST under RCM if they have a direct agreement with the landlord. In case employees incur expense on their own and take reimbursement from the entity, GST will still be applicable under RCM since the entity will be considered as recipient under GST.

The industry might see some clarity from Government on such cases, where monetary perquisites are given to employees as part of their CTC under employment contracts for rental accommodations on reimbursement basis.

B. Professionals/ sole proprietors etc. who have taken GST registrations for supplying goods /services from residential premises.